|

|||||||||||||||||||||

|

|||||||||||||||||||||

Pressing Forward and Achieving Record-Breaking Results in 2009

The Bank added 4,285 new loan clients in its roster, bringing the total number of active borrowers to 24,085. Its retail-lending brand is uniquely differentiated. It is for this reason that the Bank enjoys a higher level of customers’ patronage. Its frontliners are particularly focused on improving the loyalty of the Bank’s customers and on deepening the relationships with them.

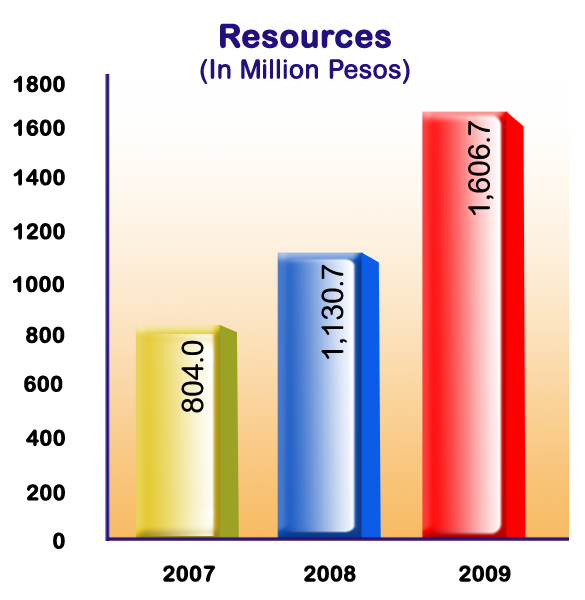

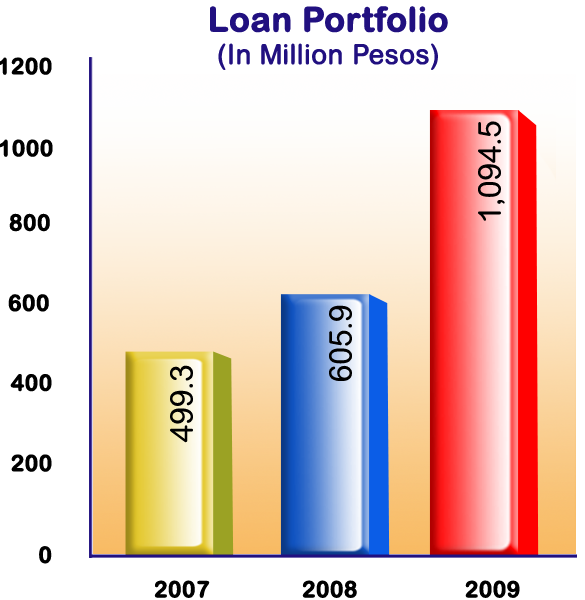

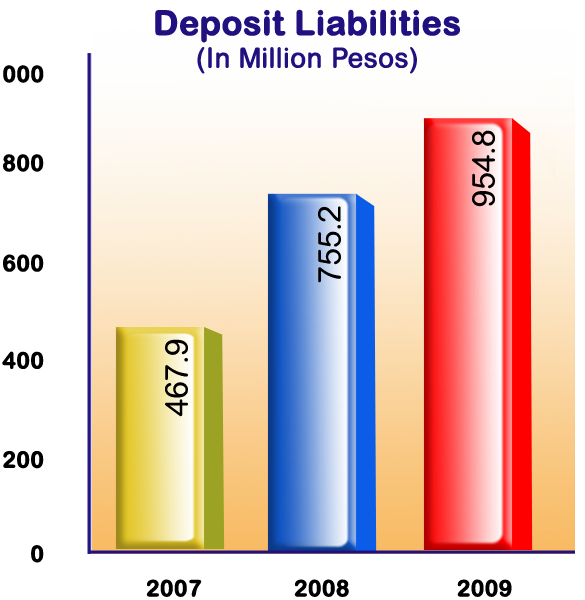

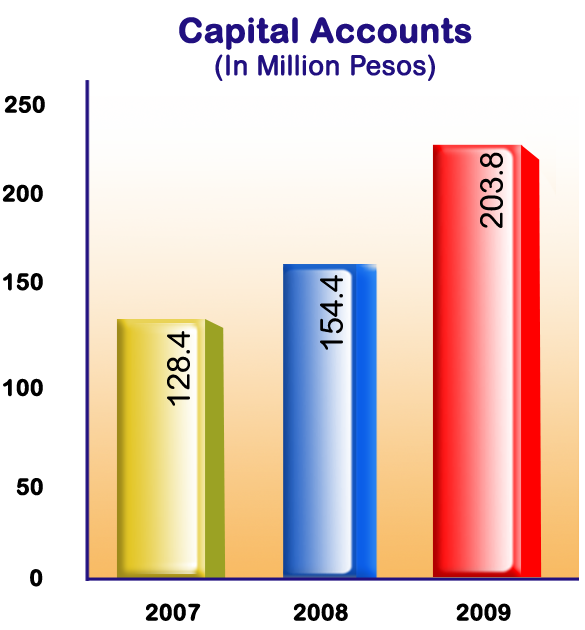

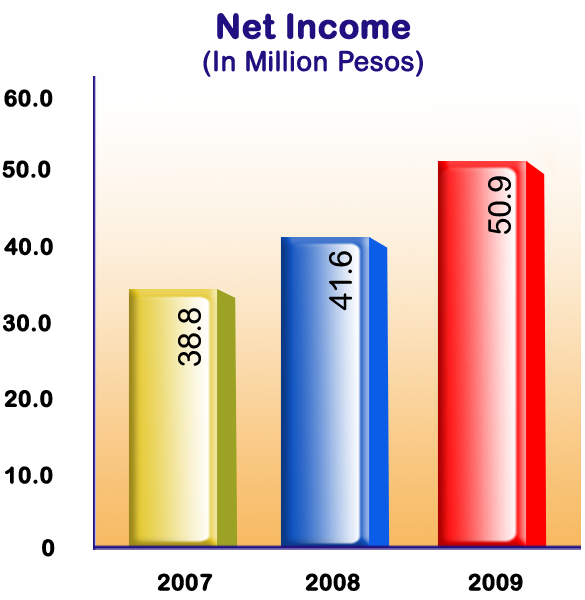

Fee-Based and Treasury Operation Aside from the impressive upswing in taking deposits and in making loans, FICOBank’s fee-based services have also gotten enough momentum during the year. For 2009, fee-based services realized a total of P12.43 million in revenue—the biggest amount that the Bank has ever collected since it started offering the same a few years back. In comparison to year-earlier output, this non-interest income, generated from the Bank’s money transfer and remittance partnerships with Western Union, G-CASH and RCBC, grew by 66.53 percent. With the cyclical levels of liquid funds for calendar year 2009, FICOBank made a P12.87 million in investment income through its placements in various banks that were able to meet the criteria set under the in-house accreditation system for financial institutions and instruments. The overall treasury yield for 2009 is 3.81 percent. Financial Performance The Bank ended year 2009 with a hefty gross income of P269.16 million. This figure represents an increase of 36.28 percent, which is twice higher than that of 2008’s growth rate of 15.72 percent. The total operating expenses of P218.30 million is 7.11 percent below the budgeted expenses of P235.00 million. The Bank’s new record of net income is in the amount of P50.86 million. It grew by 22.36 percent from the past year’s record of P41.56 million and is 13.02 percent higher than the projected bottomline. FICOBank is a better and bigger bank now than before the global financial crisis began. Its total resources as of December 31, 2009 rose to P1.61 billion from P1.13 billion a year earlier, reflecting an increase of P476 million or 42.10 percent. The cash item in the balance sheet remained nigh on P400.00 million as of year-end. This figure represents a liquidity ceiling of 41.60 percent, which is 20.60 percent above the 21-percent reserves floor (11 percent for liquidity reserves and 10 percent for regular reserves) required among banks by the Bangko Sentral ng Pilipinas to maintain. It implies a very strong liquid asset that makes FICOBank free from liquidity stress and gives the depositors more confidence on the stability and credibility of the Bank. The total loan portfolio of the Bank reached the billion-peso mark in 2009. Its outstanding balance of P1.09 billion at end-2009 indicates a growth of 80.64 percent over the preceding year’s level of P605.9 million. Although the absolute amount of non-performing loans—that is reflective of the economic condition and typhoons’ consequences—slightly increased, the Bank’s past due ratio of 4.15 percent is obviously comparable with the commercial banks and far better than the average of its peer banks. The total liabilities of the Bank, which is made up of deposit liabilities, bills payable, redeemable preferred shares, accrued expenses and other liabilities, amounted to P1.40 billion. It is 43.69 percent higher than the last year’s aggregate of P976.29 million. The bulk of these liabilities came from deposits (68.06 percent) and borrowings (26.40 percent). The Bank posted capital accounts in the amount of P203.82 million in 2009. Year-on-year analysis shows that this total amount of capital indicates an increase of P49.42 million or 32.00 percent over that of 2008’s P154.40 million. It maintained a sturdy capital structure, as both the upper and lower tiers of its capital registered remarkable increases. More importantly, the Bank’s capital adequacy ratio (CAR) throughout the year did not only comply with the BSP requirement, but did better than the minimum prescribed capital ratio of ten percent by the central bank and the Basel Accord’s standard ratio of eight percent. FICOBank’s CAR settled at 19.03 percent as of end-December 2009, higher than the overall banking industry average of 15.76 percent as of end-September 2009, as reported by BSP. With it, the Bank was able to withstand with ease the impact of the global financial crisis and economic meltdown, which peaked in the first half of 2009. Synthesis FICOBank continued to be the country’s leading cooperative bank not only in terms of financial performance, but in recognition as well. In 2009, the Bank was honored as the first Ginintuang Gawad PITAK awardee, under the cooperative rural bank category, by the Land Bank of the Philippines. FICOBank is the only cooperative bank in the country ever to achieve such distinction. Guided by its long-term strategy for transformation, the Bank’s growth initiatives and sustainability efforts generated impetus across all its banking offices; thus, giving it a greater confidence to extend its exceptional performance in 2009 into and all through 2010. |

|||||||||||||||||||||

|

|||||||||||||||||||||